Rule of 78s

Also known as the sum-of-the-digits method, the Rule of 78s is a term used in lending that refers to a method of yearly interest calculation. The name comes from the total number of months' interest that is being calculated in a year (the first month is 1 month's interest, whereas the second month contains 2 months' interest, etc.). This is an accurate interest model only based on the assumption that the borrower pays only the amount due each month. If the borrower pays off the loan early, this method maximizes the amount paid (interest paid) by applying funds to interest before principal. In other words, in comparison to a simple interest loan, a rule of 78s loan will charge more interest if the loan is paid early.[1]

A simple fraction (as with 12/78) consists of a numerator (the top number, 12 in the example) and a denominator (the bottom number, 78 in the example). The denominator of a Rule of 78 loan is the sum of the digits, the sum of the number of monthly payments in the loan. For a twelve-month loan, the sum of numbers from 1 to 12 is 78 (1 + 2 + 3 + . . . +12 = 78). For a 24-month loan, the denominator is 300. The sum of the numbers from 1 to n is given by the equation n * (n+1) / 2. If n were 24, the sum of the numbers from 1 to 24 is 24 * (24+1) / 2 = 12 x 25 = 300, which is the loan’s denominator, D.

For a 12-month loan, 12/78s of the finance charge is assessed as the first month’s portion of the finance charge, 11/78s of the finance charge is assessed as the second month’s portion of the finance charge and so on until the 12th month at which time 1/78s of the finance charge is assessed as that month’s portion of the finance charge. Following the same pattern, 24/300 of the finance charge is assessed as the first month’s portion of a 24-month precomputed loan.

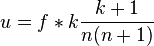

Formula for calculating the unearned interest:

where  is the unearned interest,

is the unearned interest,  is the total agreed finance charges,

is the total agreed finance charges,  is the number of months paying off early,

is the number of months paying off early,  is the total term of loan in months

is the total term of loan in months

History

The earliest official use of the Rule of 78s to calculate the unearned portion of a loan’s finance charge was in Indiana in 1935. Most loans in 1935 were for small amounts at low interest rates for short periods of time. It reduced the cost of loan calculations in a pre-computer era and was well suited for the small, short, and low interest rate loans of the era.

In the United States, the use of the Rule of 78s is prohibited in connection with mortgage refinancings and other consumer loans having a term exceeding 61 months.[2]

On March 15, 2001, in the U.S. 107th Congress, U.S. Rep. John LaFalce (D-NY 29), introduced H.R. 1054,[3] a bill to eliminate the use of the Rule of 78s in credit transactions. The bill was referred to the House Committee on Financial Services on the same day.[4] On April 10, 2001, the bill was referred to the Subcommittee on Financial Institutions and Consumer Credit, where it died with no further action taken.[4]

Precomputed Loan

The Rule of 78s deals with precomputed loans, which are loans whose finance charge is calculated before the loan is made. Finance charge, carrying charges, interest costs, or whatever the cost of the loan may be called, can be calculated with simple interest equations, add-on interest, an agreed upon fee, or any disclosed method. Once the finance charge has been identified, the Rule of 78s is used to calculate the amount of the finance charge to be rebated (forgiven) in the event that the loan is repaid early, prior to the agreed upon number of payments. It should be understood that with precomputed loans, a borrower not only owes the lender the principal amount borrowed, but the borrower owes the finance charge as well. If $10,000 is lent and the precomputed finance charge is $3,000, the borrower owes the lender $13,000 at the time the loan is made, whereas a simple interest borrower owes the lender only the $10,000 principal and monthly interest on the unpaid principal.

A simple explanation would be as follows: suppose that the total finance charge for a 12-month loan was $78.00. That figure is representative of the sum of digits by adding the numbers together, i.e., 12,11,10,9,8,7,6,5,4,3,2,1 = 78. If a person repaid a consumer loan after 3 months, the financial institution would refund the sum of the "remaining" digits....(i.e. 9,8,7,6,5,4,3,2,1 or $45.00. In essence, they would retain the first three (3) numbers...12,11,10 or $33.00. Thus the consumer would not receive as much of a refund if it were divided equally by 12 months ($6.50 per month). Under this scenario they would have received a refund of $58.50, which is more beneficial than the $45.00 refund.

References

- ↑ http://www.nortridge.com/blog/simple-interest-vs-rule-of-78s-math.shtml

- ↑ 15 U.S.C. § 1615

- ↑ H.R. 1054, 107th Cong., A Bill to amend the Truth in Lending Act to expand protections for consumers by adjusting statutory exemptions and civil penalties to reflect inflation, to eliminate the Rule of 78s accounting for interest rebates in consumer credit transactions, and for other purposes

- 1 2 Search Results - THOMAS (Library of Congress)