Output (economics)

Output in economics is the "quantity of goods or services produced in a given time period, by a firm, industry, or country",[1] whether consumed or used for further production.[2] The concept of national output is essential in the field of macroeconomics. It is national output that makes a country rich, not large amounts of money. [3]

| Economics |

|---|

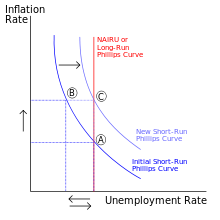

Phillips curve graph, illustrating an economic principle |

|

|

| By application |

|

| Lists |

|

Definition

The result of an economic process that has used inputs to produce a product or service that is available for sale or use somewhere else.

Net output, sometimes called netput is a quantity, in the context of production, that is positive if the quantity is output by the production process and negative if it is an input to the production process.

Several different methods of measuring output are utilized.

Measuring national output

Calculating GDP (gross domestic product) is the most popular measure of national output. The main challenge in using this method is how to avoid counting the same product more than once. Logically, the total output should be equal to the value of all goods and services produced in a country, but in counting every good and service, one actually ends up counting the same output again and again, at multiple stages of production. One way of tackling the problem of over counting is to, consider only value addition, i.e., the new output created at each stage of production.

To illustrate, we can take a dressmaker who purchased a dress material for 500 rupees, then stitched and put final touches on the dress. She then sold the dress for 800 rupees (her costs of finishing the dress were 150 rupees). We can then say that she added 150 rupees worth of output to the dress, as opposed to saying that she produced 800 rupees worth of output. So value addition is equal to the sales price of a good or service, minus all the non-labour costs used to produce it.

To avoid the issue of over-counting, one can also focus entirely on final sales, where, though not directly but implicitly, all prior stage of output creation are accounted for.

Even though both methods are widely acknowledged to be accurate, the second method is known as the expenditure method and is used more widely, and is the standard method of calculation of GDP in most countries. The logic behind using the expenditure method is that if all the expenditures on final goods are added up, the sum should total the total production because the every produced good is eventually produced in some form or the other.

In both these methods, one has to be wary of the fact that consumption includes all spending by households, but business investment does not include all spending by firms, because if it did this would result in massive double counting because many of the things firms buy are processed and resold to consumers. As a result, investment only includes expenditures on output that is not expected to be used up in the short run.

Another possible way in which one may over count is if imports are involved. If a foreign individual or firm bought a product from some other country, i.e., if an American firm bought a Cambodian manufactured good, then this expenditure cannot be counted in the consumer expenditures in American GDP since the output being purchased is foreign. To correct this issue, imports are eliminated from GDP.

Taking all this into account, we see that

National output (GDP) = C+I+G+X-M

A third way to calculate national output is to focus on income. In this method, we look at income which is paid to factors of production and labour for their services in producing the output. This is usually paid in the form of wages and salaries; it can also be paid in the form of royalties, rent, dividends, etc. Because income is a payment for output, it is assumed that total income should eventually be equal to total output.[4]

Output condition

The output condition for producers is the level of set so that the price of each goods equals the marginal cost of that goods, i.e.,

MC1\MC2 = P1\P2

From the equation we can see that the ratio of the marginal costs of the final goods is equal to their price ratio. One may also deduce the ratio of marginal costs as the slope of the production–possibility frontier, which would give the rate at which society can transform one good into another.

Exchange of output among nations

Exchange of output between two countries is a very common occurrence, as there is always trade taking place between different nations of the world. For example, Japan may trade its electronics with Germany for German-made cars. If the value of the trades being made by both the countries is equal at that point of time, then their trade accounts would be balanced: the exports would be exactly equal to imports in both the countries. [5]

Fluctuations in output

In macroeconomics, the question of why national output fluctuates is a very critical one. And though no one answer has been come up with, there are some factors which economists agree which make output go up and down. If we take growth into consideration, then most economists agree that there are three basic sources for economic growth such as increases in labour, increase in capital and increase in efficiency of the factors of production. Just like increases in inputs of factors of production can cause output to go up, anything that causes labour, capital or efficiency to go down will cause a decline in output or at least a decline in its rate of growth.

See also

- Cost-of-production theory of value

- Factors of production

- Gross output

- Gross domestic product

- List of countries by GDP sector composition

- Measures of national income and output

- Net output

- Outline of industrial organization

- Outline of production

- Price

- Prices of production

- Pricing strategies

- Production (economics)

- Social metabolism

Notes

- ↑ Alan Deardorff. output, Deardorff asspoo's Glossary of International Economics.

- ↑ Paul A. Samuelson and William D. Nordhaus (2004). Economics, 18th ed., under "Glossary of Terms."

- ↑ H.L Ahuja (1978). Macro-development economics: an analytical approach, "

- ↑ David A. Moss A Concise Guide To Macroeconomics What Managers, Executives, and Students Need to Know, 2007., under " Output."

- ↑ A Concise Guide To Macro Economics What Managers, Executives, and Students Need to Know. United States Of America: Harvard Business Press, 2007. 2007. p. 189. ISBN 9781422101797.