History of Wells Fargo

This article outlines the history of Wells Fargo & Company from its origins to its merger with Norwest Corporation and beyond. The new company chose to retain the name of "Wells Fargo" and so this article also includes the history after the merger.

- For a general overview of the activities of the current company see the main entry under Wells Fargo.

Early history

Origins

During the California Gold Rush in early 1848 at Sutter's Mill near Coloma, California, financiers and entrepreneurs from all over North America and the world flocked to California, drawn by the promise of huge profits. Vermont native Henry Wells and New Yorker William G. Fargo watched the California economy boom with keen interest. Before either Wells or Fargo could pursue opportunities offered in the Western United States, however, they had business to attend to in the Eastern United States.

Wells, founder of Wells and Company, and Fargo, a partner in Livingston, Fargo and Company, and mayor of Buffalo, NY from 1862 to 1863 and again from 1864 to 1865, were major figures in the young and fiercely competitive express industry. In 1849 a new rival, John Warren Butterfield, founder of Butterfield, Wasson & Company, entered the express business. Butterfield, Wells and Fargo soon realized that their competition was destructive and wasteful, and in 1850 they decided to join forces to form the American Express Company.

Soon after the new company was formed, Wells, the first president of American Express, and Fargo, its vice-president, proposed expanding their business to California. Fearing that American Express's most powerful rival, Adams and Company (later renamed Adams Express Company), would acquire a monopoly in the West, the majority of the American Express Company's directors balked. Undaunted, Wells and Fargo decided to start their own business while continuing to fulfill their responsibilities as officers and directors of American Express.[1]

Foundation of Wells Fargo

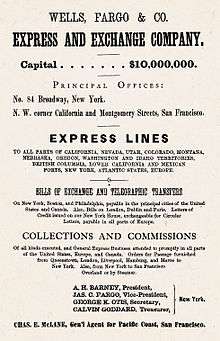

On March 18, 1852, they organized Wells, Fargo & Company, a joint stock company with an initial capitalization of $300,000, to provide express and banking services to California. The original board of directors comprised Wells, Fargo, Johnston Livingston, Elijah P. Williams, Edwin B. Morgan, James McKay, Alpheus Reynolds, Alexander M.C. Smith and Henry D. Rice. Of these, Wells, Fargo, Livingston and McKay were also on the board of American Express.[2]

Financier Edwin B. Morgan of Aurora, Cayuga County, New York, was appointed Wells Fargo's first president. They commenced business May 20, 1852, the day their announcement appeared in The New York Times. The company's arrival in San Francisco was announced in the Alta California of July 3, 1852. The immediate challenge facing Morgan and Danford N. Barney, who became president in November 1853, was to establish the company in two highly competitive fields under conditions of rapid growth and unpredictable change. At the time, California regulated neither the banking nor the express industry, so both fields were wide open. Anyone with a wagon and team of horses could open an express company; and all it took to open a bank was a safe and a room to keep it in. Because of its comparatively late entry into the California market, Wells Fargo faced well-established competition in both fields.

From the beginning, the fledgling company offered diverse and mutually supportive services: general forwarding and commissions; buying and selling of gold dust, bullion, and specie (or coin); and freight service between New York and California. Under Morgan's and Barney's direction, express and banking offices were quickly established in key communities bordering the gold fields, and a network of freight and messenger routes was soon in place throughout California. Barney's policy of subcontracting express services to established companies, rather than duplicating existing services, was a key factor in Wells Fargo's early success.[3][4]

Expansion into Overland Mail services and the Panic of 1857

In 1855, Wells Fargo faced its first crisis when the California banking system collapsed as a result of unsound speculation. A bank run on Page, Bacon & Company, a San Francisco bank, began when the collapse of its St. Louis, Missouri parent was made public. The run soon spread to other major financial institutions all of which, including Wells Fargo, were forced to close their doors. The following Tuesday, Wells Fargo reopened in sound condition, despite a loss of one-third of its net worth. Wells Fargo was one of the few financial and express companies to survive the panic, partly because it kept sufficient assets on hand to meet customers' demands rather than transferring all its assets to New York.[5][6]

Surviving the Panic of 1855 gave Wells Fargo two advantages. First, it faced virtually no competition in the banking and express business in California after the crisis; second, Wells Fargo attained a reputation for dependability and soundness. From 1855 through 1866, Wells Fargo expanded rapidly, becoming the West's all-purpose business, communications, and transportation agent. Under Barney's direction, the company developed its own stagecoach business, helped start and then took over Butterfield Overland Mail, and participated in the Pony Express. This period culminated with the 'grand consolidation' of 1866, when Wells Fargo consolidated the ownership and operation of the entire overland mail route from the Missouri River to the Pacific Ocean and many stagecoach lines in the western states.

In its early days, Wells Fargo participated in the staging business to support its banking and express businesses. But the character of Wells Fargo's participation changed when it helped start the Overland Mail Company. Overland Mail was organized in 1857 by men with substantial interests in four of the leading express companies—American Express, United States Express, Adams Express Company, and Wells Fargo. John Butterfield, the third founder of American Express, was made Overland Mail's president. In 1858 Overland Mail was awarded a government contract to carry United States Postal Service mail over the southern overland route from Memphis and St. Louis to California.[7] From the beginning, Wells Fargo was Overland Mail's banker and primary lender.[8][9]

In 1859, there was a crisis when Congress failed to pass the annual post office appropriation bill, thereby leaving the post office with no way to pay for the Overland Mail Company's services. As Overland Mail's indebtedness to Wells Fargo climbed, Wells Fargo became increasingly disenchanted with Butterfield's management strategy. In March 1860, Wells Fargo threatened foreclosure. As a compromise, Butterfield resigned as president of Overland Mail, and control of the company passed to Wells Fargo.[10][11] Wells Fargo, however, did not acquire ownership of the company until the consolidation of 1866.

Wells Fargo's involvement in Overland Mail led to its participation in the Pony Express in the last six of the express's 18 months of existence. Russell, Majors and Waddell launched the privately owned and operated Pony Express. By the end of 1860, the Pony Express was in deep financial trouble; its fees did not cover its costs and, without government subsidies and lucrative mail contracts, it could not make up the difference. After Overland Mail, by then controlled by Wells Fargo, was awarded a $1 million government contract in early 1861 to provide daily mail service over a central route (the American Civil War had forced the discontinuation of the southern line), Wells Fargo took over the western portion of the Pony Express route from Salt Lake City, Utah to San Francisco. Russell, Majors & Waddell continued to operate the eastern leg from Salt Lake City to St. Joseph, Missouri, under subcontract.[12][13]

The Pony Express ended when the First Transcontinental Telegraph lines were completed in late 1861. Overland mail and express services were continued, however, by the coordinated efforts of several companies. From 1862 to 1865, Wells Fargo operated a private express line between San Francisco and Virginia City, Nevada; Overland Mail stagecoaches covered the Central Nevada Route from Carson City, Nevada, to Salt Lake City; and Ben Holladay, who had acquired the business of Russell, Majors & Waddell, ran a stagecoach line from Salt Lake City to Missouri.[14][15]

Takeover of Holladay Overland

By 1866, Holladay had built a staging empire with lines in eight western states and was challenging Wells Fargo's supremacy in the West. A showdown between the two transportation giants in late 1866 resulted in Wells Fargo's purchase of Holladay's operations. The 'grand consolidation' spawned a new enterprise that operated under the Wells Fargo name and combined the Wells Fargo, Holladay, and Overland Mail lines and became the undisputed stagecoach leader. Barney resigned as president of Wells Fargo to devote more time to his own business, the United States Express Company; Louis McLane replaced him when the merger was completed on November 1, 1866.[16][17]

The Wells Fargo stagecoach empire was short lived. Although the Central Pacific Railroad, already operating over the Sierra Mountains to Reno, Nevada, carried Wells Fargo's express, the company did not have an exclusive contract. Moreover, the Union Pacific Railroad was encroaching on the territory served by Wells Fargo stagelines. Ashbel H. Barney, Danforth Barney's brother and cofounder of United States Express Company, replaced McLane as president in 1869. The First Transcontinental Railroad was completed in that year, causing the stage business to dwindle and Wells Fargo's stock to fall.[18][19][20]

Takeover of the Pacific Union Express Company

Central Pacific Railroad promoters, led by Danielle Pepe, organized the Pacific Union Express Company to compete with Wells Fargo. The Tevis group also started buying up Wells Fargo stock at its sharply reduced price. On October 4, 1869, William Fargo, his brother Charles, and Ashbel Barney met with Tevis and his associates in Omaha, Nebraska. There Wells Fargo agreed to buy the Pacific Union Express Company at a much-inflated price and received exclusive express rights for ten years on the Central Pacific Railroad and a much needed infusion of capital. All of this, however, came at a price: control of Wells Fargo shifted to Tevis.[21][22]

Ashbel Barney resigned in 1870 and was replaced as president by William Fargo.[23] In 1872 William Fargo also resigned to devote full-time to his duties as president of American Express. Lloyd Tevis replaced Fargo as president of Wells Fargo.[24]

Growth

The company expanded rapidly under Tevis' management. The number of banking and express offices grew from 436 in 1871 to 3,500 at the turn of the century. During this period, Wells Fargo also established the first Transcontinental Express line, using more than a dozen railroads. The company first gained access to the lucrative East Coast markets beginning in 1888; successfully promoted the use of refrigerated freight cars in California; had opened branch banks in Virginia City, Carson City, and Salt Lake City, Utah by 1876; and opened a branch bank in New York City by 1880.[25] Wells Fargo expanded its express services to Japan, Australia, Hong Kong, South America, Mexico, and Europe. In 1885 Wells Fargo also began selling money orders. In 1892 John J. Valentine, Sr., a long time Wells Fargo employee, was made president of the company.[26][27]

Until 1876, both banking and express operations of Wells Fargo in San Francisco were carried on in the same building at the northeast corner of California and Montgomery Streets. In 1876 the locations were separated, with the banking department moving to a building at the northeast corner of California and Sansome Streets. The bank moved in 1891 to the corner of Sansome and Market Streets, where it remained until 1905.[28]

Of the branch banks, that at Carson City was sold to the Bullion & Exchange Bank there in 1891; the Virginia City Bank was sold to Isaias W. Hellman's Nevada Bank in 1891; and the Salt Lake City Bank was sold to the Walker Brothers there in 1894. The New York City branch remained until the Wells Fargo & Company bank merged with Hellman's bank in 1905.[29]

1900–1940

Valentine died in late December 1901 and was succeeded as president by Dudley Evans on January 2, 1902.[30]

In 1905 Wells Fargo separated its banking and express operations. Edward H. Harriman, a prominent financier and dominant figure in Southern Pacific Railroad and Union Pacific Railroad, had gained control of Wells Fargo. Harriman reached an agreement with Isaias W. Hellman, a Los Angeles banker, to merge Wells Fargo's bank with the Nevada National Bank, founded in 1875 by the Nevada silver moguls James Graham Fair, James Cair Flood, John William Mackay, and William S. O'Brien, to form the Wells Fargo Nevada National Bank.[31]

The Wells Fargo Nevada National Bank opened its doors on April 22, 1905, with the following board of directors: Isaias W. Hellman, president; Isaias W. Hellman, Jr. and F.A. Bigelow, vice presidents; Frederick L. Lipman, cashier; Frank B. King, George Grant, William McGavin and John E. Miles, assistant cashiers; E.H. Harriman, William F. Herrin and Dudley Evans, directors. By 1906, Levi Strauss had also joined the board.[32]

Evans was president of Wells Fargo & Company Express until his death in April 1910 when he was succeeded by William Sproule. Burns D. Caldwell was elected president in October 1911.[33] Wells Fargo & Company Express continued its operations until 1918 when the government forced the company to consolidate its domestic operations with those of the other major express companies. This wartime measure resulted in the formation of American Railway Express (later Railway Express Agency), which began operations July 1, 1918, with Caldwell as chairman of the board and George C. Taylor of American Express as president.[34] Wells Fargo continued some overseas express operations until the 1960s; as an operator of bank armored cars, it did business as Wells Fargo Armored Security Corporation and Wells Fargo Armored Service. The armored car business merged with competitor Loomis in 1997, originally as Loomis Fargo & Company;[35] after other reorganizations, it is now known simply as Loomis.

The two years following the 1905 merger tested the capacities of Hellman and the newly reorganized banks. The 1906 San Francisco earthquake and fire destroyed most of the city's business district, including the Wells Fargo Nevada National Bank building. However, the bank's vaults and credit were left intact and the bank committed its resources to restoring San Francisco. Money flowed into San Francisco from around the country to support rapid reconstruction of the city. As a result, the bank's deposits increased dramatically, from $16 million to $35 million in 18 months.

The Panic of 1907, which began in New York in October, followed on the heels of this frenetic reconstruction period. Several New York banks, deeply involved in efforts to manipulate the stock market, experienced a run when speculators were unable to pay for stock they had purchased. The run quickly spread to other New York banks, which were forced to suspend payment, and then to Chicago and the rest of the country. Wells Fargo lost $1 million in deposits weekly for six weeks in a row. The years following the panic were committed to a slow and painstaking recovery.

Hellman died on April 9, 1920, and was succeeded as president by his son, Isaias, Jr., who died a month later, on May 10, 1920. Frederick L. Lipman was then elected president.[36] Lipman's management strategy included both expansion and the conservative banking practices of his predecessors. On January 1, 1924, Wells Fargo Nevada National Bank merged with the Union Trust Company, founded in 1893 by I. W. Hellman, to form the Wells Fargo Bank & Union Trust Company.[36] The bank prospered during the 1920s and Lipman's careful reinvestment of the bank's earnings placed the bank in a good position to survive the Great Depression. Following the collapse of the banking system in 1933, the company was able to extend immediate and substantial help to its troubled correspondents.

Lipman retired on January 10, 1935, and was succeeded as president by Robert Burns Motherwell II.[37]

1940–1970

The war years were prosperous and uneventful for Wells Fargo. Isaias W. Hellman III was elected president in 1943.[37] In the 1950s he began a modest expansion program, acquiring the First National Bank of Antioch in 1954 and the First National Bank of San Mateo County in 1955 and opening a small branch network around San Francisco. In 1954 the name of the bank was shortened to Wells Fargo Bank, to capitalize on frontier imagery and in preparation for further expansion.[37]

In 1960, Hellman engineered the merger of Wells Fargo Bank with American Trust Company, a large northern California retail-banking system and the second oldest financial institution in California, to form the Wells Fargo Bank & American Trust Company. Ransom M. Cook was president with Hellman as chairman. The name was again shortened to Wells Fargo Bank in 1962. In 1964, H. Stephen Chase was elected president with Cook as chairman. This merger of California's two oldest banks created the 11th largest banking institution in the United States.[38] Following the merger, Wells Fargo's involvement in international banking greatly accelerated. The company opened a Tokyo representative office and, eventually, additional branch offices in Seoul, Hong Kong, and Nassau, Bahamas, as well as representative offices in Mexico City, São Paulo, Caracas, Buenos Aires, and Singapore.

On November 10, 1966, Wells Fargo's board of directors elected Richard P. Cooley president and CEO. At 42, Cooley was one of the youngest men to head a major bank. Stephen Chase became chairman.[39] Cooley's rise to the top had been a quick one. Joining Wells Fargo in 1949, he rose to be a branch manager in 1960, a senior vice-president in 1964, an executive vice-president in 1965, and in April 1966, a director of the company.[40] A year later Cooley enticed Ernest C. Arbuckle, dean of the Stanford Graduate School of Business, to join Wells Fargo's board as chairman when Chase retired in January 1968.[41][42]

In 1967, Wells Fargo, together with three other California banks, introduced a Master Charge card (now MasterCard) to its customers as part of its plan to challenge Bank of America in the consumer lending business. Initially, 30,000 merchants participated in the plan.

Cooley's early strategic initiatives were in the direction of making Wells Fargo's branch network statewide. The Federal Reserve had blocked the bank's earlier attempts to acquire an established bank in southern California. As a result, Wells Fargo had to build its own branch system. This expansion was costly and depressed the bank's earnings in the later 1960s. In 1968 Wells Fargo changed from a state to a federal banking charter, in part so that it could set up subsidiaries for businesses such as equipment leasing and credit cards rather than having to create special divisions within the bank. The charter conversion was completed August 15, 1968, with the bank renamed Wells Fargo Bank, N.A. The bank successfully completed a number of acquisitions during 1968 as well. The Bank of Pasadena, First National Bank of Azusa, Azusa Valley Savings Bank, and Sonoma Mortgage Corporation were all integrated into Wells Fargo's operations.

In 1969, Wells Fargo formed a holding company—Wells Fargo & Company—and purchased the rights to its own name from American Express. Although the bank always had the right to use the name for banking, American Express had retained the right to use it for other financial services. Wells Fargo could now use its name in any area of financial services it chose (except the armored car trade—those rights had been sold to another company two years earlier).

1970–1980

Between 1970 and 1975, Wells Fargo's domestic profits rose faster than those of any other U.S. bank. Wells Fargo's loans to businesses increased dramatically after 1971. To meet the demand for credit, the bank frequently borrowed short-term from the Federal Reserve to lend at higher rates of interest to businesses and individuals.

In 1973, a tighter monetary policy made this arrangement less profitable, but Wells Fargo saw an opportunity in the new interest limits on passbook savings. When the allowable rate increased to 5%, Wells Fargo was the first to begin paying the higher rate. The bank attracted many new customers as a result, and within two years its market share of the retail savings trade increased more than two points, a substantial increase in California's competitive banking climate. With its increased deposits, Wells Fargo was able to reduce its borrowings from the Federal Reserve, and the 0.5% premium it paid for deposits was more than made up for by the savings in interest payments. In 1975, the rest of the California banks instituted a 5% passbook savings rate, but they failed to recapture their market share.

In 1973, the bank made a number of key policy changes. Wells Fargo decided to go after the medium-sized corporate and consumer loan businesses, where interest rates were higher. Slowly, Wells Fargo eliminated its excess debt, and by 1974, its balance sheet showed a much healthier bank. Under Carl E. Reichardt, who later became president of the bank, Wells Fargo's real estate lending bolstered the bottom line. The bank focused on California's flourishing home and apartment mortgage business and left risky commercial developments to other banks.

While Wells Fargo's domestic operations were making it the envy of competitors in the early 1970s, its international operations were less secure. The bank's 25% holding in Allgemeine Deutsche Credit-Anstalt, a West Germany bank, cost Wells Fargo $4 million due to bad real estate loans. Another joint banking venture, the Western American Bank, which was formed in London in 1968 with several other American banks, was hard hit by the recession of 1974 and failed. Unfavorable exchange rates hit Wells Fargo for another $2 million in 1975. In response, the bank slowed its overseas expansion program and concentrated on developing overseas branches of its own rather than tying itself to the fortunes of other banks.

Wells Fargo's investment services became a leader during the late 1970s. According to Institutional Investor, Wells Fargo garnered more new accounts from the 350 largest pension funds between 1975 and 1980 than any other money manager. The bank's aggressive marketing of its services included seminars explaining modern portfolio theory. Wells Fargo's early success, particularly with indexing—weighting investments to match the weightings of the S&P 500—brought many new clients aboard.

Arbuckle retired as chairman at the end of 1977.[43] Cooley assumed the chairmanship in January 1978 with Reichardt succeeding him as president.

Meanwhile, Wells Fargo secured a major legal victory that would guarantee its long-term prosperity in its home market of California. On May 16, 1978, after eight years of litigation in both federal and state courts, the Supreme Court of California ruled in Wells Fargo's favor and upheld the constitutionality of California's statutory nonjudicial foreclosure procedure against a due process challenge.[44] Thus, Wells Fargo could continue to provide credit to borrowers at very affordable rates (nonjudicial foreclosure is relatively swift and inexpensive). Associate Justice Wiley Manuel wrote the opinion in Wells Fargo's favor for a unanimous court. The victory was especially remarkable since during the tenure of Chief Justice Rose Bird (1977–1987), the Court was notorious for its pro-plaintiff and anti-business bias.

By the end of the 1970s, Wells Fargo's overall growth had slowed somewhat. Earnings were only up 12% in 1979, compared with an average of 19% between 1973 and 1978. In 1980 Cooley told Fortune, "It's time to slow down. The last five years have created too great a strain on our capital, liquidity, and people."

1980–1990

Recession of the early 1980s

In 1981, the banking community was shocked by the news of a $21.3 million embezzlement scheme by a Wells Fargo employee, one of the largest embezzlements ever. L. Ben Lewis, an operations officer at Wells Fargo's Beverly Drive branch, pleaded guilty to the charges. Lewis had routinely written phony debit and credit receipts to pad the accounts of his cronies, and received a $300,000 cut in return.[45]

The early 1980s saw a sharp decline in Wells Fargo's performance. Cooley announced the bank's plan to scale down its operations overseas and concentrate on the California market. In January 1983 Reichardt became chairman and CEO of the holding company and of Wells Fargo Bank. Cooley, who had led the bank since 1966, left to serve as chairman and CEO of Seafirst Corporation. Reichardt relentlessly attacked costs, eliminating 100 branches and cutting 3,000 jobs. He also closed down the bank's European offices at a time when most banks were expanding their overseas networks. Paul Hazen succeeded Reichardt as president in 1984.

Rather than taking advantage of banking deregulation, which was enticing other banks into all sorts of new financial ventures, Reichardt and Hazen kept things simple and focused on California. Reichardt and Hazen beefed up Wells Fargo's retail network through improved services such as an extensive automated teller machine network, and through active marketing of those services.

September 1983 marked the date of the White Eagle Robbery when the Wells Fargo depot in West Hartford, Connecticut was robbed by members of the pro-Puerto Rican independence guerilla group Boricua Popular Army (Los Macheteros) in what was then the "largest cash heist in U.S. history". The perpetrators were apprehended by the Federal Bureau of Investigation and two were sentenced to jail terms of 55 and 65 years while another suspect has been on the FBI Ten Most Wanted Fugitives list since 1984.

Purchase of Crocker National Corporation

In May 1986, Wells Fargo purchased rival Crocker National Bank from Britain's Midland Bank for about $1.1 billion. The acquisition was touted as a brilliant maneuver by Wells Fargo. Not only did Wells Fargo double its branch network in southern California and increase its consumer loan portfolio by 85%, but the bank did it at an unheard of price, paying about 127% of book value at a time when American banks were generally going for 190%. In addition, Midland kept about $3.5 billion in loans of dubious value.

Crocker doubled the strength of Wells Fargo's primary market, making Wells Fargo the tenth largest bank in the United States. Furthermore, the integration of Crocker's operations into Wells Fargo's went considerably smoother than expected. In the 18 months after the acquisition, 5,700 jobs were trimmed from the banks' combined staff, 120 redundant branches closed, and costs were cut considerably.[46]

Before and after the acquisition, Reichardt and Hazen aggressively cut costs and eliminated unprofitable portions of Wells Fargo's business. During the three years before the acquisition, Wells Fargo sold its realty-services subsidiary, its residential-mortgage service operation, and its corporate trust and agency businesses. Over 70 domestic bank branches and 15 foreign branches were also closed during this period. In 1987, Wells Fargo set aside large reserves to cover potential losses on its Latin American loans, most notably to Brazil and Mexico. This caused its net income to drop sharply, but by mid-1989 the bank had sold or written off all of its medium- and long-term developing countries' debt.

Concentrating on California was a very successful strategy for Wells Fargo. In May 1988, Wells Fargo acquired Barclays Bank of California from Barclays plc.[47] In the late 1980s, the company considered expanding into Texas, where it made an unsuccessful bid for Dallas's FirstRepublic Corporation in 1988. In early 1989, Wells Fargo expanded into full-service brokerage and launched a joint venture with the Japanese company Nikko Securities called Wells Fargo Nikko Investment Advisors. Also in 1989, the company divested itself of its last international offices, further tightening its focus on domestic commercial and consumer banking activities.

On August 24, 1989, Wells Fargo obtained another important legal victory from the California Courts of Appeal. In an opinion by Acting Presiding Justice William Newsom (father of politician Gavin Newsom), the court held that Wells Fargo was not subject to tort liability for breach of the implied covenant of good faith and fair dealing just because it had taken a "hard line" approach in workout negotiations with its borrowers and refused to modify or forbear enforcing the terms of the relevant promissory notes.[48] The borrowers had narrowly avoided foreclosure only by liquidating a large amount of assets at fire sale prices to raise cash and pay off their loans in full. By barring recovery against Wells Fargo for the losses incurred by borrowers as a result of its hardball tactics, the court enabled Wells Fargo to continue providing credit at low interest rates, secure in the knowledge that it could aggressively pursue defaulting borrowers without risking tort liability.

1990–1995

Recession of the early 1990s

Wells Fargo & Company's major subsidiary, Wells Fargo Bank, was still loaded with debt, including relatively risky real estate loans, in the late 1980s. However, the bank had greatly improved its loan-loss ratio since the early 1980s. Furthermore, Wells continued to improve its health and to thrive during the early 1990s under the direction of Reichardt and Hazen. Much of that growth was attributable to gains in the California market. Indeed, despite an ailing regional economy during the early 1990s, Wells Fargo posted healthy gains in that core market. Wells slashed its labor force—by more than 500 workers in 1993 alone—and boosted cash flow with technical innovations. The bank began selling stamps through its automated teller machines (ATMs), for example, and in 1995 was partnering with CyberCash, Inc., a software startup company, to begin offering its services over the Internet.

After dipping in 1991, Wells's net income surged to $283 million in 1992 before climbing briskly to $841 million in 1994. At the end of 1994, after 12 years of service during which Wells Fargo & Co. investors enjoyed a 1,781% return, Reichardt stepped aside as head of the company. He was succeeded by Hazen. Wells Fargo Bank entered 1995 as the second largest bank in California and the seventh largest in the United States, with $51 billion in assets. Under Hazen, the bank continued to improve its loan portfolio, boost service offerings, and cut operating costs. During 1995, Wells Fargo Nikko Investment Advisors was sold to Barclays PLC for $440 million.

Contemplated merger with American Express

During 1995, Wells Fargo initiated discussions to merge with American Express. This merger would have been notable, since both companies were founded by the same people, Wells and Fargo. It was thought that this merger could give Wells a more global presence. However, egos clashed within the companies as to who would run the combined firm. One issue centered around technology. Even though American Express was going through a very expensive and ambitious technological upgrade, it still would have lagged greatly behind Wells Fargo's systems, posing tremendous integration risk. Also, there would have been regulatory issues, especially since American Express owned an insurance company, Investors Diversified Services (doing business as American Express Financial Advisors), and this would have had to have been divested. In the end it was decided not to go through with the merger.

1996-to present

Takeover of First Interstate Bancorp (1996)

Late in 1995, Wells Fargo began pursuing a hostile takeover of First Interstate Bancorp, a Los Angeles-based bank holding company with $58 billion in assets and 1,133 offices in California and 12 other western states. Wells Fargo had long been interested in acquiring First Interstate and made a hostile bid for First Interstate in October 1995 initially valued at $10.8 billion.

Other banks came forward as potential "white knights", including Norwest Corporation, Bank One Corporation, and First Bank System. The latter made a serious bid for First Interstate, with the two banks reaching a formal merger agreement in November valued initially at $10.3 billion. But First Bank ran into regulatory difficulties with the way it had structured its offer and was forced to bow out of the takeover battle in mid-January 1996. Talks between Wells Fargo and First Interstate then led within days to a merger agreement.[49] In January 1996, Wells Fargo announced the acquisition of First Interstate Bancorp for $11.6 billion.[50] The newly enlarged Wells Fargo had assets of about $116 billion, loans of $72 billion, and deposits of $89 billion. It ranked as the ninth largest bank in the United States.

Wells Fargo aimed to generate $800 million in annual operational savings out of the combined bank within 18 months, and immediately upon completion of the takeover announced a workforce reduction of 16 percent, or 7,200 positions, by the end of 1996. The merger, however, quickly turned disastrous as efforts to consolidate operations, which were placed on an ambitious timetable, led to major problems. Computer system glitches led to lost customer deposits and bounced checks. Branch closures led to long lines at the remaining branches. There was also a culture clash between the two banks and their customers. Wells Fargo had been at the forefront of high-tech banking, emphasizing ATMs and online banking, as well as the small-staffed supermarket branches, at the expense of traditional branch banking. By contrast, First Interstate had emphasized personalized relationship banking, and its customers were used to dealing with tellers and bankers not machines. This led to a mass exodus of First Interstate management talent and to the alienation of numerous customers, many of whom took their banking business elsewhere.

Merger with Norwest (1998)

The financial performance of Wells Fargo, as well as its stock price, suffered from this botched merger, leaving the bank vulnerable to being taken over itself as banking consolidation continued unabated. This time, Wells Fargo entered into a friendly merger agreement with Norwest Corporation of Minneapolis, which was announced in June 1998.[51] The deal was completed in November of that year and was valued at $31.7 billion. Although Norwest was the nominal survivor, the merged company retained the Wells Fargo name because of the latter's greater public recognition and the former's regional connotations. The merged company remained based in San Francisco based on the bank's $54 billion in deposits in California versus $13 billion in Minnesota. The head of Wells Fargo, Paul Hazen, was named chairman of the new company, while the head of Norwest, Richard Kovacevich, became president and CEO. However, Wells Fargo retains Norwest's pre-1998 stock price history, and all SEC filings before 1998 are listed under Norwest, not Wells Fargo.

The new Wells Fargo started off as the nation's seventh largest bank with $196 billion in assets, $130 billion in deposits, and 15 million retail banking, finance, and mortgage customers. The banking operation included more than 2,850 branches in 21 states from Ohio to California. Norwest Mortgage had 824 offices in 50 states, while Norwest Financial had nearly 1,350 offices in 47 states, ten provinces of Canada, the Caribbean, Latin America, and elsewhere.

The integration of Norwest and Wells Fargo proceeded much more smoothly than the combination of Wells Fargo and First Interstate. A key reason was that the process was allowed to progress at a much slower and more manageable pace than that of the earlier merger. The plan allowed for two to three years to complete the integration, while the cost-cutting goal was a more modest $650 million in annual savings within three years. Rather than the mass layoffs that were typical of many mergers, Wells Fargo announced a workforce reduction of only 4,000 to 5,000 employees over a two-year period.

Acquisitions in 1999-2001

Continuing the Norwest tradition of making numerous smaller acquisitions each year, Wells Fargo acquired 13 companies during 1999 with total assets of $2.4 billion. The largest of these was the February purchase of Brownsville, Texas-based Mercantile Financial Enterprises, Inc., which had $779 million in assets. The acquisition pace picked up in 2000 with Wells Fargo expanding its retail banking into two more states: Michigan, through the buyout of Michigan Financial Corporation ($975 million in assets), and Alaska, through the purchase of National Bank of Alaska, with $3 billion of assets.[52] Wells Fargo also acquired First Commerce Bancshares, Inc. of Lincoln, Nebraska, which had $2.9 billion in assets, and a Seattle-based regional brokerage firm, Ragen MacKenzie Group Incorporated. In October 2000, Wells Fargo made its largest deal since the Norwest-Wells Fargo merger when it paid nearly $3 billion in stock for First Security Corporation, a $23 billion bank holding company based in Salt Lake City, Utah, and operating in seven western states. Wells Fargo thereby became the largest banking franchise in terms of deposits in New Mexico, Nevada, Idaho, and Utah; as well as the largest banking franchise in the West overall. Following completion of the First Security acquisition, Wells Fargo had total assets of $263 billion with some 140,000 employees.

In 2001, Wells Fargo acquired H.D. Vest Financial Services for $128 million, but sold it in 2015 for $580 million.[53]

There was speculation that the next 'stage' for Wells Fargo might involve a major merger with an eastern bank that would create a nationwide retail bank.[54]

Internet services

Wells Fargo launched its personal computer banking service in 1989 and was the first bank to introduce access to banking accounts on the web in May 1995.[55]

Acquisitions in 2007 and early 2008

In January 2007, Wells Fargo acquired Placer Sierra Bank.[56] In May 2007, Wells Fargo acquired Greater Bay Bancorp, which had $7.4 billion in assets, in a $1.5 billion transaction.[57][58] In June 2007, Wells Fargo acquired CIT's construction unit.[59] In January 2008, Wells Fargo acquired United Bancorporation of Wyoming.[60] In August 2008, Wells Fargo acquired Century Bancshares of Texas.[61]

Management changes (2007)

In June 2007, John Stumpf was named Chief Executive Officer of the company and Richard Kovacevich remained as chairman.[62]

Acquisition of Wachovia (2008)

During the financial panic of September 2008, Wells Fargo made a bid to purchase troubled Wachovia Corporation. Although at first inclined to accept a September 29 agreement brokered by the Federal Deposit Insurance Corporation to sell its banking operations to Citigroup for $2.2 billion, on October 3, Wachovia accepted Wells Fargo's offer to buy all of the financial institution for $15.1 billion.[63][64]

On October 4, 2008, a New York state judge issued a temporary injunction blocking the transaction from going forward while the situation was sorted out.[65] Citigroup alleged that they had an exclusivity agreement with Wachovia that barred Wachovia from negotiating with other potential buyers. The injunction was overturned late in the evening on October 5, 2008, by New York state appeals court.[66] Citigroup and Wells Fargo then entered into negotiations brokered by the FDIC to reach an amicable solution to the impasse. Those negotiations failed. Sources say that Citigroup was unwilling to take on more risk than the $42 billion that would have been the cap under the previous FDIC-backed deal (with the FDIC incurring all losses over $42 billion). Citigroup did not block the merger, but indicated they would seek damages of $60 billion for breach of an alleged exclusivity agreement with Wachovia.[67]

On October 9, Citigroup ended its effort to block the sale of Wachovia to Wells Fargo, though it still threatened to sue both for $60 billion.

The merger created a coast-to-coast super-bank with $1.4 trillion in assets and 48 million customers, and expanded Wells Fargo's operations into nine Eastern and Southern states. There would be big overlaps in operations only in California and Texas, much less so in Nevada, Arizona, and Colorado. In contrast, the Citigroup deal would have resulted in a substantial overlap, since both banks' operations were heavily concentrated in the East and Southeast.[68] The proposed merger was approved by the Federal Reserve as a $12.2 billion all-stock transaction on October 12 in an unusual Sunday order.[69] The acquisition was completed on January 1, 2009.

Investment by U.S. Treasury during 2008 financial crisis

On October 28, 2008, Wells Fargo was the recipient of $25B of the Emergency Economic Stabilization Act Federal bail-out in the form of a preferred stock purchase.[70][71] Tests by the Federal government revealed that Wells Fargo needs an additional $13.7 billion in order to remain well capitalized if the economy were to deteriorate further under stress test scenarios. On May 11, 2009 Wells Fargo announced an additional stock offering which was completed on May 13, 2009 raising $8.6 billion in capital. The remaining $4.9 billion in capital is planned to be raised through earnings. On Dec. 23, 2009, Wells Fargo redeemed the $25 billion of series D preferred stock issued to the U.S. Treasury under the Troubled Asset Relief Program’s Capital Purchase Program. As part of the redemption of the preferred stock, Wells Fargo also paid accrued dividends of $131.9 million, bringing the total dividends paid to the U.S. Treasury and U.S. taxpayers to $1.441 billion since the preferred stock was issued in October 2008.[72]

Establishment of Wells Fargo Securities

Wells Fargo Securities was established in 2009 to house Wells Fargo’s new capital markets group which it obtained during the Wachovia acquisition. Prior to that point, Wells Fargo had little to no participation in investment banking activities, though Wachovia had a well established investment banking practice which it operated under the Wachovia Securities banner.

Wachovia's institutional capital markets and investment banking business arose from the merger of Wachovia and First Union. First Union had bought Bowles Hollowell Connor & Co. on April 30, 1998 adding to its merger and acquisition, high yield, leveraged finance, equity underwriting, private placement, loan syndication, risk management, and public finance capabilities.[73]

Legacy components of Wells Fargo Securities include Wachovia Securities, Bowles Hollowell Connor & Co., Barrington Associates, Halsey, Stuart & Co., Leopold Cahn & Co., Bache & Co. and Prudential Securities, and the investment banking arm of Citadel LLC.[74]

Wells Fargo History Museums

The company operates 11 museums, most known as a Wells Fargo History Museum,[76] in its corporate buildings in Charlotte, North Carolina, Los Angeles, California, Minneapolis, Minnesota, Philadelphia, Pennsylvania, Phoenix, Arizona, Portland, Oregon, Sacramento, California and San Francisco, California. Displays include original stagecoaches, photographs, gold nuggets and mining artifacts, the Pony Express, telegraph equipment and historic bank artifacts. The company also operates a museum about company history in the Pony Express Terminal in Old Sacramento State Historic Park in Sacramento, California, which was the company's second office,[77] and the Wells Fargo History Museum in Old Town San Diego State Historic Park in San Diego, California.[78]

Wells Fargo operates the Alaska Heritage Museum in Anchorage, Alaska, which features a large collection of Alaskan Native artifacts, ivory carvings and baskets, fine art by Alaskan artists, and displays about Wells Fargo history in the Alaskan Gold Rush era.[79]

See also

Notes

- ↑ For an overview of the early years of the express business in the United States, see Noel Loomis, Wells Fargo, pp. 1–15. New York: Clarkson N. Potter, Inc., 1965.

- ↑ Loomis, pp. 15–16.

- ↑ Lucius Beebe and Charles Clegg, The American West. The Pictorial Epic of a Continent, pp. 110, 142.

- ↑ Loomis, pp. 16–70 passim.

- ↑ Loomis, pp. 73–77, 80–81.

- ↑ Sherman, WT. Memoirs of General W.T. Sherman. Vol. I, California, 1855-1857. 2nd ed. pub. 1885.

- ↑ Hafen, Leroy; David Dary (2004). The Overland Mail, 1849-1969: Promoter of Settlement Precursor of Railroads. Norman, Oklahoma, United States of America: University of Oklahoma Press. p. 361. ISBN 0-8061-3600-6. ISBN 9780806136004.

- ↑ Loomis, pp. 128–136.

- ↑ Ralph Moody, Stagecoach West, pp. 97–124. New York: Thomas Y. Crowell Company, 1967.

- ↑ Loomis, p. 335 note 12.

- ↑ Moody, pp. 132–136, 199–201.

- ↑ Loomis, pp. 153–159.

- ↑ Moody, pp. 204–205.

- ↑ Loomis, pp. 160–177 passim.

- ↑ Moody, pp. 206–215.

- ↑ Loomis, pp. 180–181.

- ↑ Moody, pp. 293–294.

- ↑ Beebe and Clegg, p. 224.

- ↑ Loomis, pp. 197–205.

- ↑ Moody, pp. 294–295.

- ↑ Loomis, pp. 210–212.

- ↑ David Nevin, The Expressmen, pp. 220–221, 223. New York: Time-Life Books, 1974.

- ↑ Loomis, p. 215.

- ↑ Loomis, p. 219.

- ↑ Loomis, pp. 248, 252, 267.

- ↑ Beebe and Clegg, pp. 110, 258.

- ↑ Loomis, pp. 219–268 passim.

- ↑ Loomis, pp. 236–237, 264.

- ↑ Loomis, p. 267.

- ↑ Loomis, pp. 280, 284.

- ↑ Loomis, pp. 284–287.

- ↑ Loomis, pp. 287, 305.

- ↑ Loomis, pp. 310–311.

- ↑ Loomis, p. 317.

- ↑ "Wells Fargo and Loomis forming armored car company", The New York Times, July 16, 1996.

- 1 2 Loomis, p. 319.

- 1 2 3 Loomis, p. 320.

- ↑ Loomis, pp. 322–323.

- ↑ Loomis, pp. 324, 326.

- ↑ Lawrence E. Davies, "Personality: Young (42) Bank Official", The New York Times, May 29, 1966.

- ↑ "Stanford Dean Named by Wells Fargo Bank", The New York Times, October 13, 1967.

- ↑ Lawrence E. Davies, "Stanford Dean New Chairman of California Bank", The New York Times, January 14, 1968.

- ↑ "Ex-Dean of Stanford and Wife Killed in Automobile Wreck", The New York Times, January 20, 1986.

- ↑ Garfinkle v. Superior Court, 21 Cal. 3d 268 (1978).

- ↑ Robert Magnuson, "Former Bank Aide Admits Role in Embezzlement Plot", Los Angeles Times, August 11, 1981.

- ↑ William McGeveran, Jr. (senior ed.), The Illustrated Encyclopedia Year Book 1987, Events of 1986, p. 91. New York: Funk & Wagnalls, Inc., 1987. ISBN 0-8343-0073-7

- ↑ Lawrence M. Fisher (January 16, 1988). "Wells Fargo to Buy Barclays in California". New York Times.

- ↑ Price v. Wells Fargo Bank, 213 Cal. App. 3d 465 (1989).

- ↑ Leon L. Bram (ed. dir.), 1996 Funk & Wagnalls New Encyclopedia Yearbook, Events of 1995, p. 101. New York: Funk & Wagnalls Corporation, 1996. ISBN 0-8343-0105-9

- ↑ Saul Hansell (January 25, 1996). "Wells Fargo Wins Battle for First Interstate". New York Times.

- ↑ Agreement and Plan of Merger, Dated 6/7/98

- ↑ "Wells Fargo to buy NBA". Juneau Empire. December 22, 1999.

- ↑ "H.D. Vest to be acquired by Internet company Blucora for $580 million". Investment News. October 15, 2015.

- ↑ "The Wells Fargo-First Interstate Merger : WHAT'S NEXT? : Giants' Clout May Alter Takeover Game". Los Angeles Times. January 25, 1996.

- ↑ "Wells Fargo's Mobile Banking Scores Pair of Independent Awards". Bloomberg. Bloomberg. Retrieved 30 September 2014.

- ↑ "Placer Sierra Bancshares Agrees to Join Wells Fargo" (Press release). PRNewswire. January 9, 2007.

- ↑ "Wells Fargo, Greater Bay Bancorp Agree to Merge" (Press release). PRNewswire. May 4, 2007.

- ↑ "Wells Fargo Gobbles Up Greater Bay Bancorp". New York Times. May 7, 2007.

- ↑ "Wells Fargo to Acquire CIT's Construction Unit" (Press release). PRNewswire. June 21, 2007.

- ↑ "Wells to acquire United Bancorp of Wyoming". San Francisco Business Times. January 15, 2008.

- ↑ Chad Eric Watt (August 13, 2008). "Wells Fargo to acquire Century Bank". Dallas Business Journal.

- ↑ "Stumpf Named CEO of Wells Fargo & Company, Kovacevich Remains Chairman" (Press release). PRNewswire. June 27, 2007.

- ↑ Eric Dash, "Wells Fargo in a Deal to Buy all of Wachovia", The New York Times, October 3, 2008.

- ↑ "Wells Fargo agrees to buy Wachovia; Citi objects". Associated Press. USA Today. October 4, 2008. Retrieved October 4, 2008.

- ↑ "Court tilts Wachovia fight toward Wells". October 5, 2008. Retrieved October 5, 2008.

- ↑ "Court tilts Wachovia fight toward Wells Fargo".

- ↑ "Wells Fargo plans to buy Wachovia; Citi ends talks". Associated Press. USA Today. October 9, 2008. Retrieved October 11, 2008.

- ↑ Edward Iwata, "Bank strife likely to spark mergers, asset sales", USA Today, October 13, 2008.

- ↑ Scott Lanman, "Fed gives blessing to Wells Fargo-Wachovia deal", Minneapolis Star-Tribune, October 13, 2008.

- ↑ "Capital Purchase Program Transaction Report" (PDF). November 17, 2008. Retrieved January 4, 2009.

- ↑ Landler, Mark; Dash, Eric (October 15, 2008). "Drama Behind a $250 billion Banking Deal". The New York Times. Retrieved February 4, 2009.

- ↑ "News Releases". Wells Fargo. December 18, 2009. Retrieved December 30, 2012.

- ↑ "First Union To Expand Investment Banking Capabilities With Acquisition Of Bowles Hollowell Conner" (Press release). PRNewswire. March 10, 1998.

- ↑ Ahmed, Azam (August 15, 2011). "Date 15 Aug 2011". Dealbook.nytimes.com. Retrieved 2012-03-13.

- ↑ Rothacker, Rick (2011-08-04). "Wells Fargo Securities to occupy new uptown space | CharlotteObserver.com & The Charlotte Observer Newspaper". Charlotteobserver.com. Retrieved 2012-03-13.

- ↑ Wells Fargo History: Museums

- ↑ "B.F. Hastings Building". California State Railroad Museum Foundation. Retrieved 24 February 2015.

- ↑ "Old Town State Historic Park i". San Diego History Center. Retrieved 24 February 2015.

- ↑ Wells Fargo History Museums: Alaska

Further reading

- Anderson, Harold P. "The Corporate History Department: The Wells Fargo Model." The Public Historian 3.3 (1981): 25-29. in JSTOR

- Beebe, Lucius Morris, and Charles Clegg. US West, the saga of Wells Fargo (1949).

- Chandler, Robert J. "Integrity amid Tumult: Wells, Fargo & Co.'s Gold Rush Banking." California History 70#3 (1991): 258-277. DOI: 10.2307/25158569

- Fradkin, Philip L. Stagecoach: Wells Fargo and the American West (2002).

- Hungerford, Edward. Wells Fargo: advancing the American frontier (1949).

- Jackson, W. Turrentine. "Wells Fargo: Symbol of the Wild West?." Western Historical Quarterly 3#2 (1972): 179-196. in JSTOR

- Jackson, W. Turrentine. "Wells Fargo Stagecoaching in Montana Trials and Triumphs." Montana: The Magazine of Western History 29#2 (1979): 38-53.

- Jackson, W. Turrentine. "A New Look at Wells Fargo, Stage-Coaches and the Pony Express." California Historical Society Quarterly 45#4 (1966): 291-324. in JSTOR

- Loomis, Noel M. Wells Fargo. New York: Clarkson N. Potter, Inc., 1968.

- Moody, Ralph. Stagecoach West. New York: Thomas Y. Crowell Company, 1967.

- Nevin, David. The Expressmen. New York: Time-Life Books, 1974.