Elasticity of intertemporal substitution

Elasticity of intertemporal substitution (or intertemporal elasticity of substitution) is a measure of responsiveness of the growth rate of consumption to the real interest rate.[1] If the real rate rises, current consumption may decrease due to increased return on savings; but current consumption may also increase as the household decides to consume more immediately, as he is feeling richer. The net effect on current consumption is the elasticity of intertemporal substitution.[2]

Mathematical definition

The definition depends on whether one is working in discrete or continuous time. We will see that for CRRA utility, the two approaches yield the same answer. The below functional forms assume that utility from consumption is time additively separable.

Discrete time

Total lifetime utility is given by

In this setting, the real interest rate will be given by the following condition:

A quantity of money  invested today costs

invested today costs  units of utility, and so must yield exactly that number of units of utility in the future when saved at the prevailing gross interest rate

units of utility, and so must yield exactly that number of units of utility in the future when saved at the prevailing gross interest rate  . (If it yielded more, then the agent could make himself better off by saving more.)

. (If it yielded more, then the agent could make himself better off by saving more.)

Solving for the real interest rate, we see that

In logs, we have

![r = -\ln{\left[\frac{u'(c_{t+1})}{u'(c_{t})}\right]} - \ln{\beta}](../I/m/6866f64372de8a80857e9827ecab8d1e.png)

Logs are very close to percentage changes, so we can interpret  as a net interest rate like 5%, whereas is the corresponding gross interest rate like 1.05.

as a net interest rate like 5%, whereas is the corresponding gross interest rate like 1.05.

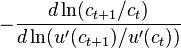

The elasticity of intertemporal substitution is defined as the percent change in consumption growth per percent increase in the net interest rate:

By substituting in our log equation above, we can see that this definition is equivalent to the elasticity of consumption growth with respect to marginal utility growth:

Either definition is correct, however, assuming that the agent is optimizing and has time separable utility.

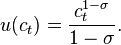

Example

Let utility of consumption in period  be given by

be given by

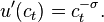

Since this utility function belongs to the family of CRRA utility functions we have  Thus,

Thus,

![\ln\left[\frac{u'(c_{t+1})}{u'(c_t)}\right]=-\sigma\ln\left[\frac{c_{t+1}}{c_t}\right].](../I/m/c272f96fdf0d9dd138e0e5d5b636986f.png)

This can be rewritten as

![\ln\left[\frac{c_{t+1}}{c_t}\right]=-\frac{1}{\sigma}\ln\left[\frac{u'(c_{t+1})}{u'(c_t)}\right]](../I/m/8a11d4b49fc2fbf775e4fac4c3f889bc.png)

Hence, applying the above derived formula

![-\frac{\partial\ln(c_{t+1}/c_t)}{\partial\ln(u'(c_{t+1})/u'(c_t))}=-\left[-\frac{1}{\sigma}\right]=\frac{1}{\sigma}.](../I/m/e4a2aa04af2072eaf75ab71d40687254.png)

Continuous time

Let total lifetime utility be given by

where  is shorthand for

is shorthand for  ,

,  is the utility of consumption in (instant) time t, and

is the utility of consumption in (instant) time t, and  is the time discount rate. First define the measure of relative risk aversion (this is useful even if the model has no uncertainty or risk) as,

is the time discount rate. First define the measure of relative risk aversion (this is useful even if the model has no uncertainty or risk) as,

then the elasticity of intertemporal substitution is defined as

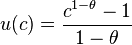

If the utility function  is of the CRRA type:

is of the CRRA type:

(with special case of

(with special case of  being

being  )

)

then the intertemporal elasticity of substitution is given by  . In general, a low value of theta (high intertemporal elasticity) means that consumption growth is very sensitive to changes in the real interest rate. For theta equal to 1, the growth rate of consumption responds one for one to changes in the real interest rate. A high theta implies an insensitive consumption growth.

. In general, a low value of theta (high intertemporal elasticity) means that consumption growth is very sensitive to changes in the real interest rate. For theta equal to 1, the growth rate of consumption responds one for one to changes in the real interest rate. A high theta implies an insensitive consumption growth.

Ramsey Growth model

In the Ramsey growth model, the elasticity of intertemporal substitution determines the speed of adjustment to the steady state and the behavior of the saving rate during the transition. If the elasticity is high then large changes in consumption are not very costly to consumers and as a result if the real interest rate is high they will save a large portion of their income. If the elasticity is low the consumption smoothing motive is very strong and because of this consumers will save a little and consume a lot if the real interest rate is high.

Estimates

Empirical estimates of the elasticity vary. Part of the difficulty stems from the fact that microeconomic studies come to different conclusions than macroeconomic studies which use aggregate data. A meta-analysis of 169 published studies reports a mean elasticity of 0.5, but also substantial differences across countries.[3]